Executive Intelligence. Industrial Risk. Geopolitics.

Strategic Sparring

for Decision-Makers

Risk intelligence across technology, law, markets and power dynamics.

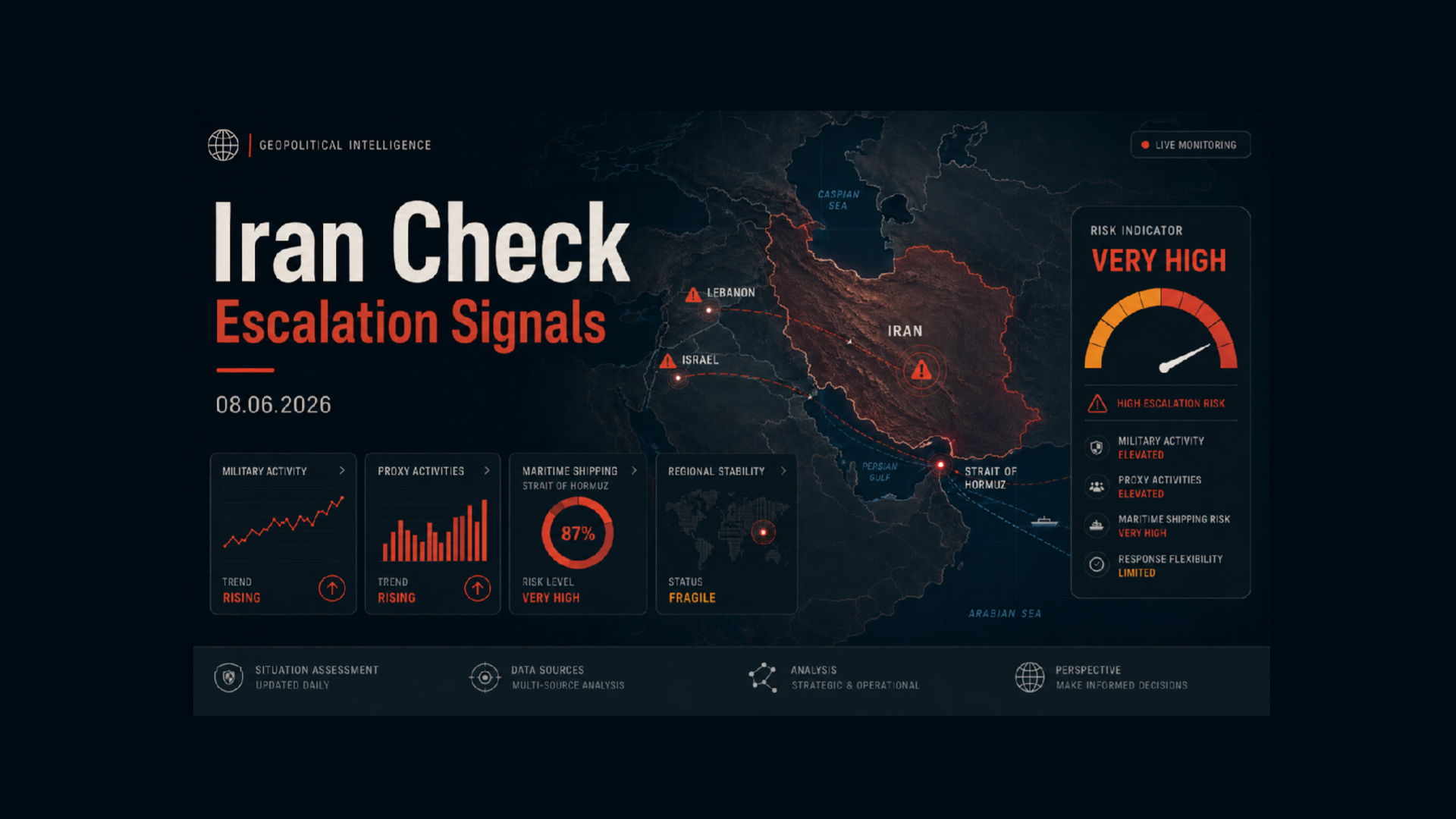

This escalation radar summarizes five relevant signals as of July 16, 2026. The focus is on verifiable statements by official actors, confirmed events and monitoring sources with potential impact on energy prices, supply chains, markets, maritime security, aviation and regional stability.

The key change: on July 16, Iran is no longer only speaking about control or blockade, but explicitly declares the Strait of Hormuz a “red line”. Any attempt to break this control militarily or operationally is therefore marked as a direct escalation trigger.

The United States is no longer targeting only coastal, naval and Hormuz-adjacent assets, but is expanding its strikes to targets around Tehran and other Iranian provinces. This shifts the escalation from a maritime security operation to a broader military pressure campaign against Iran.

Oil prices ease slightly on July 16, but remain near one-month highs. At the same time, the number of Hormuz transits is falling sharply. For companies, this is dangerous: the market is sending a calming signal while transport, insurance and routing risks remain operationally elevated.

| Actor | Type | Severity | Status | Source / verification status | Business impact |

|---|---|---|---|---|---|

| United States / Iran / IRGC / Kharg Island / northern Iran | Expansion of US strikes, blockade enforcement and Iranian counterattacks | Critical · Level 5/5 | The US-Iran situation escalated again on July 16, 2026. AP reports that the United States expanded its airstrikes into northern Iran and hit targets around Tehran and in other provinces. In addition, an oil tanker near Kharg Island was stopped or disabled after allegedly attempting to bypass the US blockade. According to AP, Iran responded with missile and drone attacks on US allies or US-aligned targets in Bahrain, Jordan and Kuwait. The power dynamic: Washington is shifting the operation from pure Hormuz security to military pressure on Iranian infrastructure and blockade enforcement. Tehran is trying to raise the cost of this US line immediately through attacks on allies and regional bases. This makes the escalation broader, deeper and harder to control than it was on July 14. | Confirmed by AP News, 16.07.2026. Verification status: confirmed for the expansion of US strikes, blockade enforcement against a vessel near Kharg Island and Iranian counterattacks on US-aligned targets; the exact damage picture, military strike effects and political escalation limits remain partly unclear. | Critical business impact on Gulf exposure, energy prices, insurance, security costs, military risk premiums, expat safety, site continuity, banking and payment risks, crisis logistics, and companies with offices, suppliers or customers in Bahrain, Jordan, Kuwait, Qatar, Oman, Saudi Arabia and the United Arab Emirates. |

| Iran / Hormuz / IRGC / United States / regional energy exports | Iran declares Hormuz a “red line” and threatens further escalation | Critical · Level 5/5 | Iran is hardening its political and operational threat logic on July 16. Reuters reports that Tehran explicitly described the Strait of Hormuz as a “red line” and said it would resist US measures until the end. Iranian officials insist on full control over the strait and warn that any attempt to break that control will be answered with force. In addition, Iran warns neighboring states against supporting US military operations and threatens retaliation against any cooperation. The power dynamic: Iran is trying to define Hormuz not merely as a transit route, but as a sovereignty and deterrence space. The United States treats the same space as an international corridor that must be kept open militarily. Hormuz therefore becomes the core of an open authority conflict: who controls the chokepoint, who defines legal passage, and who bears the cost of any attempted breakthrough? | Confirmed by Reuters, 16.07.2026. Verification status: confirmed for Iran’s “red line” statement on Hormuz, the threat against supporters of US operations and Iran’s self-definition as the controlling power in the chokepoint; it remains open how far Iran can enforce the threat practically and durably. | Critical business impact on oil and LNG transport, tanker routing, container traffic, war-risk premiums, insurability, charter costs, spot rates, delivery times, port planning, energy procurement, hedging, commodity prices and companies with Gulf, energy, chemicals, fertilizer, air freight or heavy industry exposure. |

| Hormuz / oil market / LNG / tankers / shipowners | Oil prices ease slightly, but Hormuz transits fall sharply | High to critical · Level 4/5 | The operational picture in energy and shipping remains contradictory on July 16. Reuters reports that oil prices eased slightly even though US-Iran conflict risks remain high. According to Reuters, Brent fell to USD 84.37 per barrel and WTI to USD 79.42, while both prices remained near one-month highs. At the same time, the number of Hormuz transits fell sharply: Reuters cites only seven vessels on Wednesday versus thirteen the previous day. The power dynamic: markets are not pricing in a full blockade in the short term, but shipowners and operators are already acting more cautiously. This is especially important for companies: price relief does not mean operational all-clear when physical passage, insurance and routing are tightening at the same time. | Confirmed by Reuters, 16.07.2026. Verification status: confirmed for slightly lower oil prices amid continued elevated conflict risk, declining Hormuz transits and prices near one-month highs; it remains open whether the market is underestimating the operational chokepoint risk. | High to critical business impact on energy procurement, hedging, commodity prices, delivery times, charter costs, insurability, LNG availability, just-in-time supply chains, port planning, transport budgets and companies with energy-intensive production, chemicals, fertilizer, logistics or air freight structures. |

| Lebanon / Israel / Hezbollah / United States | Rome talks concluded, pilot-zone guidelines assessed positively, Hezbollah remains the blocking point | High to critical · Level 4/5 | The Lebanon situation shows a mixed picture on July 16: diplomatic progress combined with strategic blockage. Reuters reports that Lebanon and Israel concluded another round of US-brokered talks in Rome. The talks concerned the implementation of pilot zones, the disarmament of militant groups, the deployment of Lebanese troops and a phased Israeli withdrawal. According to Reuters, a US official described the talks as “productive and positive”. At the same time, the core conflict remains unresolved: Israel continues to insist on a 10-km buffer zone, Lebanon demands withdrawal, and Hezbollah rejects disarmament without broader political conditions. The power dynamic: Washington and Israel want to create stability through disarmament, pilot zones and state control. Lebanon needs sovereignty and withdrawal, but has only limited control over Hezbollah’s armed power. The talks are therefore a de-escalation signal, but not yet a durable breakthrough. | Confirmed by Reuters, 15./16.07.2026. Verification status: confirmed for the conclusion of the Rome talks, the pilot-zone guidelines, the positive US tone and the unresolved disputes over Israeli withdrawal, buffer zone and Hezbollah disarmament; it remains open whether technical implementation is politically enforceable. | High relevance for Lebanon and northern Israel exposure, security planning, evacuation, insurance, humanitarian logistics, regional supply chains, border risks, political risk premiums and companies with personnel, partners or projects in the Levant. |

| EASA / Iran / Iraq / Lebanon / Gulf region | Active aviation warnings amid missile, drone, air-defense and GNSS risk | Critical · Level 5/5 | The aviation situation remains critical on July 16 and is further burdened by renewed US-Iran escalation. EASA lists active Conflict Zone Advisories for the airspaces of Iran, Iraq and Lebanon, as well as for the Persian Gulf and Gulf of Oman. According to EASA, entries for the Persian Gulf and Gulf of Oman as well as for Lebanon and Iraq are active and valid until August 31, 2026. The current escalation confirms this risk picture: US strikes, Iranian counterattacks, air-defense activity, military movements around Hormuz and possible GNSS/navigation disruptions increase risks for flight routes, air freight and business travel. The operational takeaway: aviation and air freight risk must not be inferred from oil price or shipping signals alone. | Confirmed by EASA Conflict Zones Advisories, accessed 16.07.2026. Verification status: confirmed for active EASA warning logic and continued risk assessment for Iran, Iraq, Lebanon, the Persian Gulf and the Gulf of Oman; specific airline route decisions remain dependent on operators, states, insurers and daily risk assessments. | Critical business impact on air freight, airlines, rerouting, spare-parts supply chains, business travel, crisis logistics, airport risk, just-in-time supply chains, insurance, personnel movement and companies with Middle East, Gulf or Asia-Europe air-corridor exposure. |

The central escalation node on July 16, 2026 lies in the shift from blockade and fee logic to open red-line logic. Compared with July 14, Iran has explicitly marked the Strait of Hormuz as a red line, while the United States is expanding its strikes into northern Iran and enforcing the blockade against individual vessels. Hormuz is therefore no longer only a dispute over maritime order, but a direct escalation trigger.

Operationally, the situation has become more deceptive for companies because the market looks slightly calmer in the short term, while physical passage and risk assessment are tightening at the same time. Oil prices are easing slightly, but remain near one-month highs, the number of Hormuz transits is falling sharply, and shipowners, insurers and operators must continue to price in blockade, routing, insurance and escalation risks. The decisive issue is now not only what oil costs, but whether passage, protection, insurance and time windows remain planable at all.

Politically, the situation remains especially dangerous because military escalation and partial diplomatic progress are running side by side. Washington is increasing military pressure on Iran and treating blockade breaches as enforceable risks. Tehran declares Hormuz a red line and threatens supporters of US operations with retaliation. In parallel, the Rome talks on Lebanon and Israel provide a de-escalation signal, but remain fragile due to Hezbollah’s disarmament, Israeli buffer zones and the question of state control in southern Lebanon.

The five most important signals for a European business risk picture are: Iran’s declaration of the Strait of Hormuz as a “red line”, the expansion of US strikes into northern Iran, blockade enforcement against a vessel near Kharg Island, declining Hormuz transits despite only slightly lower oil prices, and concluded Rome talks on Lebanon-Israel pilot zones while EASA warnings remain active for Iran, Iraq, Lebanon and the Gulf region.

Note: This assessment was created with support from our Geo AI. AI can make mistakes. This document serves as a radar for potential escalation signals and does not replace a fully verified final intelligence assessment.

What decision-makers should watch now — before proxy escalation becomes a cost, compliance or supply-chain shock.

This 17-page executive briefing translates Iran’s proxy network into concrete business risks: energy price exposure, maritime chokepoints, war-risk premiums, sanctions, shadow fleets, supply-chain disruption and early-warning indicators for board-level decisions.